A TRIS allows Australians who have reached preservation age to access their super while continuing to work.

2 June, 2026

The only requirement for a TRIS is age

First Financial Team

There has been much discussion recently about the TRIS (Transition to Retirement Income Stream), and in April this year, the team published an article explaining the concept.

Since then, our advisers have been actively speaking with many clients about the prospect of entering into a TRIS and the requirements.

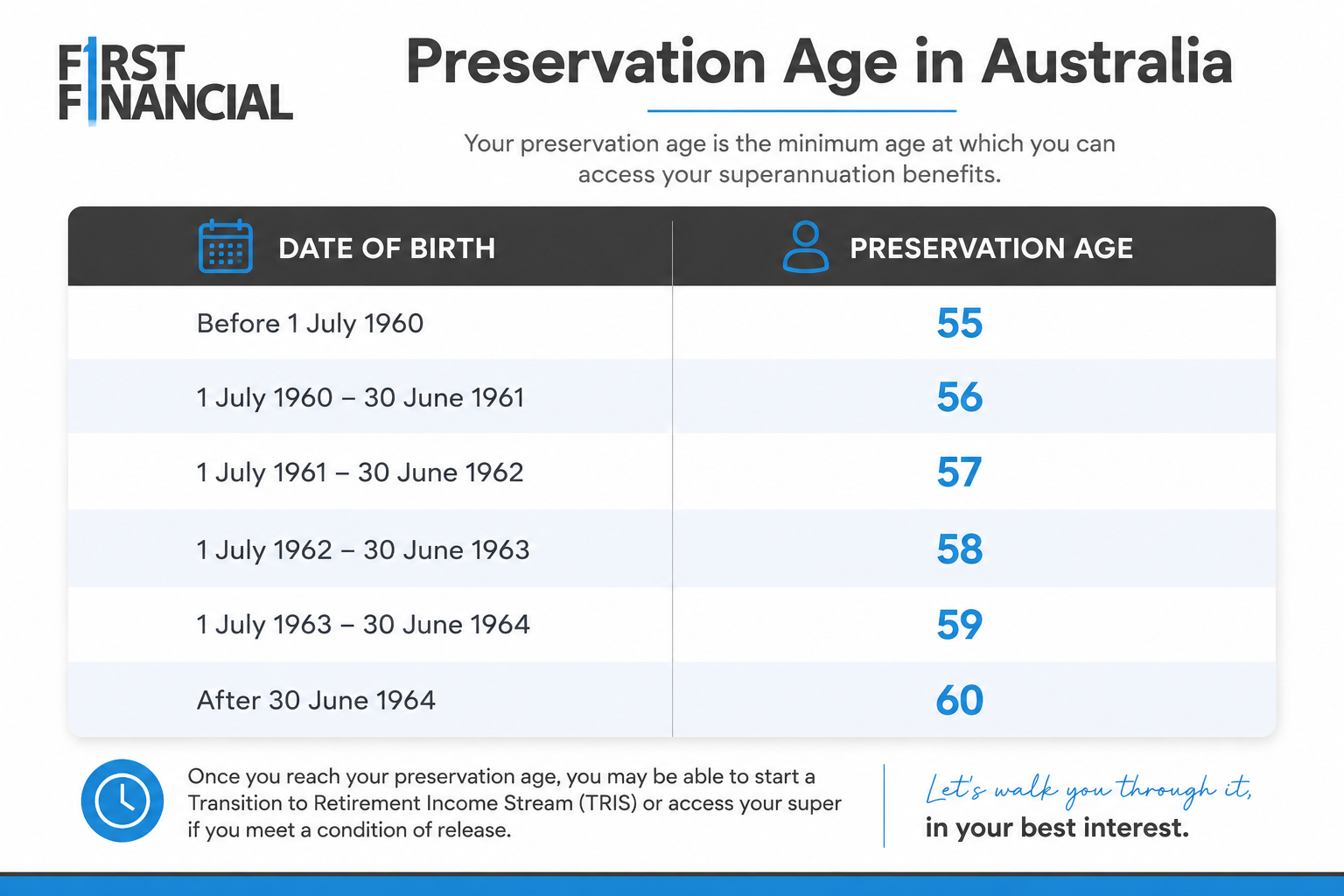

The fact is that the only requirement is age. So, what is it? To enter into a TRIS, you must have reached preservation age.

A Transition to Retirement Income Stream (TRIS), also known as a Transition to Retirement (TTR), was introduced to help individuals gradually transition from full-time employment to retirement while maintaining their lifestyle as much as possible. With many Aussies living longer and current cost-of-living pressures, a TRIS is becoming increasingly popular.

“The only requirement to commence a Transition to Retirement Income Stream is reaching your preservation age.”

Who benefits from a TRIS?

A TRIS is purposely designed for people who have reached their preservation age but are not ready to fully retire. It can be particularly beneficial for:

- Individuals who want to reduce their working hours without reducing their income.

- People who are looking to boost their super balance before retirement.

- Higher-income earners seeking tax efficiencies.

- Workers who are planning a gradual transition into retirement rather than stopping work abruptly.

You do not need to meet all the conditions of release, such as retirement, to commence a TRIS. Reaching preservation age is sufficient.

How does a TRIS work?

When you start a TRIS, a portion of your superannuation balance is transferred from your accumulation account into a pension account. You can then receive regular income payments while continuing to work. The government sets both minimum and maximum withdrawal limits:

- Minimum annual withdrawal: 4% of the account balance for those under age 65.

- Maximum annual withdrawal: 10% of the account balance.

For example, if you transfer $400,000 into a TRIS:

- Minimum annual pension payment: $16,000

- Maximum annual pension payment: $40,000

These payments can be made monthly, quarterly, half-yearly or annually, depending on your needs.

“A TRIS can help Australians reduce their working hours while maintaining their income and continuing to build their retirement savings.”

How do I initiate a TRIS, and what are the primary advantages?

To initiate a TRIS, the requirements are relatively straightforward:

- Reach your preservation age (currently 60 for most Australians).

- Have a superannuation balance available to transfer into the pension account.

- Be a member of a super fund that offers TRIS pensions.

- Complete the relevant application paperwork with your super fund or adviser.

The primary advantage of a TRIS is maintaining income while reducing time spent working. Most people entering a TRIS gradually reduce their 5-day work week to 4 or 3 days and replace the reduced income with payments from their superannuation. TRIS pension payments are generally tax-free when received from a taxed super fund. This can create opportunities to salary sacrifice additional income into super while replacing cash flow through pension payments.

What is the disadvantage of a TRIS?

Like any strategy, a TRIS must be right for the circumstances, and in some cases, it may not be the best option. Importantly, you are drawing funds from your superannuation to cover the reduced income from working less. Additionally, earnings on assets supporting a TRIS generally remain taxable within the fund at up to 15% until a full retirement condition of release is met. There is also extra administration: although it is minimal, there is additional paperwork and ongoing monitoring to ensure minimum and maximum withdrawal requirements are met.

How much super do I need for a TRIS to be viable?

While there is no legislated minimum balance, a TRIS becomes more effective when there is enough capital to generate meaningful pension payments. As a general guide:

- Under $100,000 – Often provides limited benefits due to small withdrawal amounts.

- $200,000–$300,000 – May provide useful supplementary income.

- $400,000–$600,000+ Often allows greater flexibility and can support more sophisticated salary sacrifice strategies.

- $750,000+ Can provide significant income supplementation while maintaining strong retirement savings.

For example, someone with a $500,000 TRIS account could withdraw between $20,000 and $50,000 per year under current rules. The viability of a TRIS depends on several factors:

- Current salary and tax bracket.

- Desired reduction in work hours.

- Existing super balance.

- Planned retirement age.

- Contribution levels.

- Investment performance.

A TRIS can be a useful tool for Australians seeking greater flexibility in the years leading up to retirement. However, because the benefits depend heavily on individual circumstances, obtaining personalised financial advice before implementing a TRIS strategy is essential to ensure it aligns with your retirement and lifestyle goals.

The team at First Financial comprises financial experts who help hundreds of Australians retire well and make informed, intelligent financial decisions. We cover everything from retirement and financial advice, investment and wealth management, superannuation and SMSF, insurance, tax, aged care, legal and lending services.

Contact us for holistic, well-rounded financial management strategies.

Key takeaways

Many people use a TRIS to reduce their working hours and replace lost income with pension payments from their superannuation.

TRIS strategies can offer tax advantages and may help boost retirement savings through salary sacrifice arrangements.

Professional financial advice is important, as the benefits of a TRIS depend on your income, super balance, retirement goals and overall financial circumstances.

YOUR FINANCIAL JOURNEY

Building your financial future

Every client journey begins with a conversation. We look closely at where you are now, what matters to you, and what’s possible. Then we structure our advice to match.

Financial

Roadmap

A clear, personalised path to your financial goals.

Tax

Efficiency

Proactive strategies to maximise your tax savings.

Personalised

Investing

Tailored plans aligned with your goals and risk profile.

Ongoing

Support

Regular guidance to keep your plan on track.

CLIENT STORY

John

Life Stage:

Retired business owner

Background:

After decades of running a successful pharmacy, John sought financial guidance to simplify decision-making and support long-term planning.

- Navigated the sale of a long-held business

- Wanted simple, honest advice after burnout

- Needed a hands-on adviser he could talk to

- Desired financial guidance aligned with lifestyle goals

- Crafted a strategy that supports relaxed, post-work life

- Offered approachable, plain-English advice

- Maintained an ongoing, trustworthy relationship

- Provided flexibility with investments and cash flow

“I feel genuinely supported by First Financial. I can ask anything, and there’s no pressure, just clear advice and real care. The money’s growing, I’m not stressed about it, and I feel completely at ease for the first time. I don’t miss work, but I’d miss the support I get from First Financial.”

CLIENT STORY

Jan

Life Stage:

Retired

Background:

Jan's husband managed the finances until entering aged care. Jan gradually stepped into the financial picture with First Financial’s support.

- Needed financial guidance after business sale

- Lacked experience managing complex finances

- Sought consistent income and long-term structure

- Wanted a familiar, reliable relationship

- Provided long-term support through several transitions

- Helped structure income reliably for retirement

- Empowered Jan through education and reassurance

- Delivered calm advice through both grief and growth

“The money just comes in. I don’t have to think about it. And I know they’re always there. They’ve always been there in the background, just quietly making things work.”

CLIENT STORY

Graeme and Craig

Life Stage:

Retired and semi-retired

Background:

Referred by friends who were helped through aged care, Craig sought secure financial guidance after inheriting funds.

- Invest inheritance securely without high risk

- Maintain a modest lifestyle with confidence

- Building trust for someone new to advice

- Accessible, personalised advice

- Provided a low-risk strategy with regular income

- Reassured with steady, market-aware updates

- Established trust through responsiveness and warmth

- Delivered calm, expert support through all transitions

“We feel very secure with First Financial, the income just comes in, and we know everything is being looked after. It’s not just safe, it’s smart. We’ve recommended them to others because we genuinely believe in the team.”

CLIENT STORY

Tim and Adam

Life Stage:

Early retirement and working professional

Background:

When Tim received an overseas medical settlement, he and Adam had just 14 days left in a 90-day window. They needed clear guidance, fast. A referral led them to First Financial.

- Only two weeks left to meet urgent legal and financial deadlines

- Wanted to preserve capital while setting up income for the future

- Needed a plan that supported both retirement and ongoing work

- Hoped to find advice that felt personal, not transactional

- Managed every moving piece, from legal documents to super rollovers

- Designed a strategy that supported both Tim’s retirement and Adam’s career

- Offered clear guidance with steady follow-through, with no stress or pressure

- Built in ethical investing and flexibility, without sacrificing performance

“We’re in totally different life stages, but First Financial built a strategy that supports us both. From urgent legal steps to ethical investing, they handled every detail with calm, care, and real expertise. It’s financial freedom without compromise, and we couldn’t have done it without them.”

CLIENT STORY

Lyn

Life Stage:

Retired widow

Background:

Lyn stepped into financial management for the first time after her husband's passing. With patience and care, First Financial supported her through grief, learning, and empowerment.

- Had never managed finances before

- Was overwhelmed after her husband’s passing

- Needed plain-English explanations and patience

- Sought emotional support and practical clarity

- Offered caring, respectful advice at her pace

- Rebuilt confidence with diagrams, stories, and reassurance

- Supported gradual decision-making around retirement

- Remained a trusted constant through major transitions

“After my husband passed, I was completely unsure where to start. First Financial gave me the space to learn, to ask questions, to grow confident. They drew a diagram that I still have. And now, I sleep well at night knowing I’ve got someone in my corner.”

CLIENT STORY

Larry and Virginia

Life Stage:

Newly retired

Background:

As retirement neared, Larry and Virginia were ready to enjoy travel, family, and freedom, without uncertainty. A friend recommended First Financial, and from the first meeting, they had a clear plan, a safety net, and people they trusted.

- Wanted to travel and enjoy retirement without second-guessing finances

- Needed a structured income plan with buffers for the unexpected

- Valued guidance that felt honest and human, not overcomplicated

- Needed people they could call and count on

- Created a reliable income stream with a set-aside safety net for the unexpected

- Gave them the freedom to travel and spend meaningfully with family

- Kept advice simple, thoughtful, and tailored to what mattered to them

- Built a lasting partnership based on trust

“We’ve travelled the world, Europe, Sri Lanka, Vietnam, without once stressing about the money. They made everything feel simple and gave us the confidence to live well. We feel secure because we know exactly where we stand, and that peace of mind means everything.”

Meet our advisers

Frequently Asked Questions

What is a Transition to Retirement Income Stream (TRIS)?

A Transition to Retirement Income Stream (TRIS) allows you to access part of your superannuation while continuing to work. It is designed to help Australians gradually transition from full-time work into retirement.

Who is eligible to start a TRIS?

The only requirement to commence a TRIS is that you have reached your preservation age. You do not need to retire or meet any other condition of release.

Can I reduce my working hours and maintain my income with a TRIS?

Yes. Many people use a TRIS to reduce their working days while supplementing their income with regular superannuation payments.

How much can I withdraw from a TRIS each year?

If you are under age 65, you must withdraw at least 4% of your TRIS account balance each year and no more than 10%. The exact amount will depend on your account balance and financial needs.

What are the main benefits of a TRIS?

A TRIS can help you maintain your lifestyle while working fewer hours. It may also create tax-effective opportunities to boost your super through salary sacrifice arrangements.

Are there any disadvantages to a TRIS?

A TRIS involves drawing money from your retirement savings earlier than planned. Earnings on assets supporting a TRIS are generally taxed within the fund until you meet a full retirement condition of release.

Why should I seek advice from First Financial before starting a TRIS?

The effectiveness of a TRIS depends on factors such as your income, super balance, retirement goals and tax position. First Financial can assess your individual circumstances and determine whether a TRIS strategy is likely to improve your long-term retirement outcomes.

How can First Financial help me implement a TRIS strategy?

First Financial provides personalised retirement and superannuation advice to help ensure a TRIS aligns with your lifestyle and financial objectives. Their advisers can guide you through the setup process and help you maximise the strategy’s potential benefits.